Why Texas Royalty Brokers?

sellers

Buyers

State Specific Guides

Resources

Mineral Rights Loan vs Selling Mineral Rights

Are you considering a mineral rights loan?

The decision between taking out a loan against mineral rights or selling them outright is an important choice.

In this article, we’ll provide you with a comprehensive guide to help you make the right decision for your financial future. We’ll weigh the pros and cons of a mineral rights loan versus selling mineral rights.

DO NOT get a mineral rights loan until you have fully read this article. We’re going to explain why a mineral rights loan is often a trap and provide alternative options.

Additionally, we’ll highlight potential pitfalls to avoid, such as first right of refusal clauses, ensuring that you don’t fall victim to common traps and maximize the value of your mineral assets.

This article will serve as your roadmap to navigating the decision to take a mineral rights loan or sell mineral rights.

What is a Mineral Rights Loan

A mineral rights loan is a type of financing where your mineral rights, such as oil and gas royalties, are used as collateral for a cash loan. These loans are typically offered to mineral owners who want to access the value of their property without selling it outright.

How Mineral Rights Loans Work

Here’s how the process typically works:

-

Collateral: The lender places a lien on your mineral rights or royalty income. In some cases, you may be required to assign a portion or all of your royalty income directly to the lender.

-

Loan Amount: Usually based on current royalty income or projected future value. Offers often equal one to three years of royalty income.

-

Terms: These loans often come with high interest rates, balloon payments, and short repayment periods. Most are set to be paid back within 12 to 36 months.

-

Repayment: Payments are often deducted directly from your royalty checks. In other cases, the entire loan plus interest is due at the end of the term.

-

Default Risk: If royalty income declines or stops, you could be in default even if you made all payments on time. Many lenders include strict default language in the contract.

Common Requirements

-

Clear title to the mineral rights

-

Consistent royalty income history

-

First Right of Refusal (FRoR) if you try to sell later

-

Assignment of royalty payments or lien on title

-

Personal guarantees in some cases

Before moving forward with a mineral rights loan, it’s important to understand what you’re agreeing to.

These loans can seem attractive when you need fast cash, but they often come with complex terms and hidden risks. From liens and personal guarantees to restrictions on future sales, the fine print matters. Understanding these terms upfront will help you avoid surprises and make a more informed decision about whether a loan or a sale is the better path forward.

Basic Risks and Pitfalls of Mineral Rights Loans

Mineral rights loans may seem like a quick solution for accessing cash without selling your property. But many of these loans come with serious risks that are often buried in the fine print. Understanding these risks upfront is critical before signing anything.

High Interest Rate Mineral Rights Loans

Interest rates on mineral rights loans are often much higher than traditional loans. This is due to the perceived risk of fluctuating royalty income. Over time, the interest adds up quickly and significantly reduces the total value you receive from the loan.

Short Terms and Balloon Payments

Most mineral rights loans are structured with repayment periods between 12 and 36 months. Some require monthly payments while others delay repayment until the end of the term. In those cases, the entire amount is due in one lump sum. This is called a balloon payment. If your royalty income slows down or stops, you may not be able to make the final payment.

Trigger Clauses and Default Risk

Loan contracts often include terms that allow the lender to call the loan due early. These are known as trigger clauses and can include things like:

-

A change in operator

-

A drop in production

-

A delay in royalty payments

-

Attempting to sell your minerals without lender approval

Any one of these could trigger a default, even if you have made every payment on time. Once a default is triggered, the full loan balance may become due immediately.

Predatory Contract Terms

Some loan agreements include aggressive legal language that heavily favors the lender. Watch for these red flags:

-

Default interest: If you default, the interest rate can increase automatically

-

Prepayment penalties: You may be charged extra for trying to pay off the loan early

-

Recorded liens: The lender may file a lien on your property that limits your ability to sell or restructure later

Mineral rights loans are complex financial agreements. The risks are not always obvious upfront.

Reading the contract carefully and understanding how these terms work is the only way to avoid unintended consequences. In many cases, owners find that other options provide a cleaner and more reliable path forward.

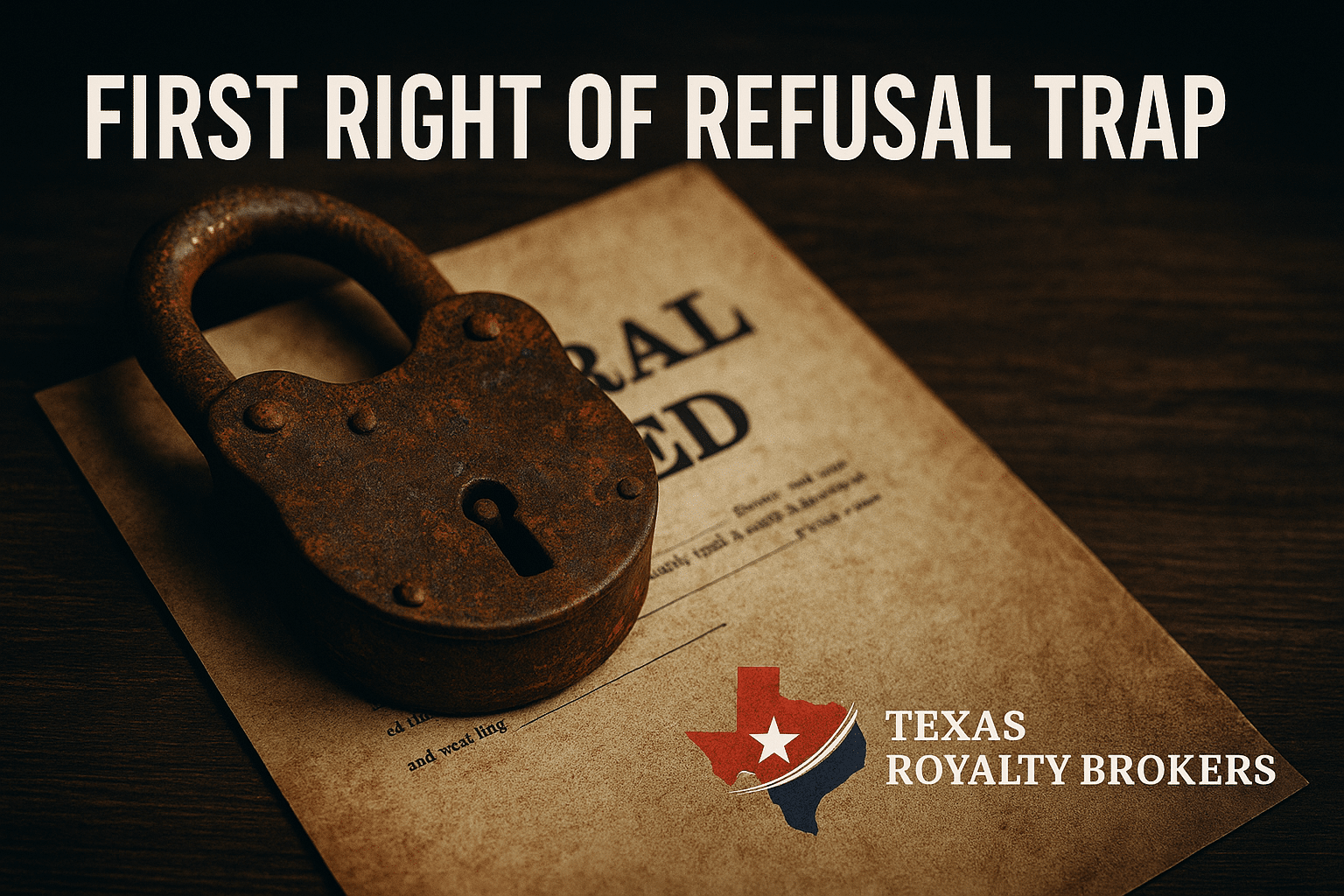

Understanding First Right of Refusal

A First Right of Refusal (FRoR) is one of the most dangerous clauses found in mineral rights loan agreements. If this clause is in your contract, it will prevent you from selling your mineral rights freely. It will also reduce the value of your property and limit your options going forward.

What It Means

A First Right of Refusal gives the lender the legal right to match any future offer you receive to sell your mineral rights. This means that before you can sell to another party, you must first present the offer to the lender and give them the chance to buy your rights under the same terms.

Why This Hurts You

This clause completely removes your ability to conduct a normal, competitive sale. Mineral buyers know their offer might just be used as a placeholder for the lender to match. As a result, they are less likely to offer their best price. In many cases, they will not make an offer at all. This drives down demand and ultimately lowers the sale price you can get.

It Will Block a Future Sale

We cannot stress this enough. If you sign a loan agreement with a First Right of Refusal clause, you may not be able to sell your mineral rights at all. Even if you find a buyer, the lender can delay or block the process. Many sales fall apart when buyers learn that the mineral rights are tied up in a first right of refusal clause.

How to Spot These Clauses

Look for language in the contract that says things like:

-

“Lender shall have the first right to purchase”

-

“Borrower agrees to provide written notice of any third-party offer”

-

“Lender shall have the right to match any bona fide offer”

These phrases are legal triggers that should raise red flags.

How Texas Royalty Brokers Handles a First Right of Refusal

When a client comes to us and mentions they have a loan, we ask two questions:

- Who is the lender?

- Does your loan include a first right of refusal?

Once the mineral owners confirms it’s that certain lender, and that their loan includes a first right of refusal, we will not list the mineral rights for sale. Why?

The rights right of refusal kills the value of the mineral rights. The vast majority of buyers will not bid on mineral rights when they have a first right of refusal. It complicates things and it wastes everyone’s time.

If you take out a mineral rights loan, you need to fully understand that you may not have the ability to sell the mineral rights. If you do, it will be for a significantly discounted price.

Don’t do it.

Mineral Rights Loan Traps and Red Flags

Even when you try to pay off a mineral rights loan, lenders may still block or delay your ability to sell. Some of these actions are questionable at best and can leave your mineral rights tied up long after the loan should have been resolved.

Below are the most common traps to look out for.

Payoff Amount Traps

Getting a clear payoff amount should be simple, but it often is not. Some lenders avoid giving a written payoff letter. Others send one with an expiration window that is unrealistic. If you do not pay within that window, they may refuse to honor it or add unexpected fees.

Some payoff letters include vague charges or inflated fees without any breakdown. Without a clean and final number, you cannot close the deal, and the uncertainty may cause your buyer to walk away.

Industry Experience: At Texas Royalty Brokers we have seen a specific lender who will refuse to provide a payoff amount. This kills the deal and you can’t sell.

No Communication Trap

It is common for lenders to stop responding once you begin trying to resolve the loan or prepare for a sale. Emails and phone calls go unanswered. Payoff requests sit idle.

This silence is not accidental. Some lenders use lack of communication to stall the process and keep control of your minerals. They know that if they do nothing, your sale cannot go through.

Once again, we have seen this happen on multiple occasions. The lender will simply stop responding to all communication and prevent you from doing anything. They respond very quickly when you’re taking the loan, but as soon as you are ready to sell or pay off the loan they stop responding.

Lien Release Trap

Even if you pay the loan in full, the lender may delay filing the lien release. This document is critical. Until it is filed and recorded, your mineral rights remain clouded. Buyers will not proceed without it.

In some cases, lenders will claim they sent it when they have not. Others will require extra steps that were never part of the original agreement. If the lien is never released, you may be forced to go to court to clear the title.

Industry Tip: A mineral buyer WILL NOT close until there is a lien release in hand. The lender will simply decline to provide one and prevent you from selling.

Delay Trap

Some lenders delay intentionally. They know most buyers have a timeline. By slowing down the process just enough, the lender can cause the buyer to back out. This lets them hold onto control of the mineral rights and avoid giving up their position.

These delays are not always obvious. You may think the deal is moving forward while the lender quietly waits, creating just enough friction to kill the sale.

If a lender is not responding, refusing to issue a payoff letter, or holding up the lien release, take it seriously. These are not minor inconveniences. They are strategies that prevent you from selling your property. Always keep written records of your communication, and be prepared to involve legal counsel if the lender becomes uncooperative.

Mineral Rights Loan Solutions

Whether you are considering a mineral rights loan or already locked into one, there are better ways to access the value of your mineral rights without sacrificing long-term upside or control.

Below are two situations with real, actionable solutions.

If You Have Not Taken Mineral Rights a Loan Yet

If you are thinking about taking out a mineral rights loan, stop and explore other options first.

These loans come with serious risks and often cost more than you realize. The smartest move in most cases is to sell a portion of your mineral rights.

Sell a Portion Instead of Taking a Loan

This approach gives you immediate cash while allowing you to retain some ownership for future upside. The portion you keep stays clean and unencumbered by a loan, lien, or contract. You maintain full control and avoid the interest, penalties, and legal traps that come with loan agreements.

Whether you choose to sell at Texas Royalty Brokers or not, we strongly recommend selling a portion and not taking out a mineral rights loan. Most mineral owners can sell 50% of their mineral rights, meet their cash needs, and keep their remaining mineral rights.

Other Options to Consider

If selling a portion is not your first choice, you still have better alternatives than a mineral rights loan:

-

Use a home equity line of credit (HELOC)

-

Use a credit card for short-term needs

-

Borrow against other assets with more favorable terms

In nearly every case, these options are safer and more transparent than signing a mineral rights loan.

If You Already Took a Mineral Rights Loan

If you have already signed a mineral rights loan agreement, the best path forward is to eliminate the loan as soon as possible.

The longer it stays in place, the more problems it can cause, especially if you try to sell mineral rights later.

Option One: Pay Off the Loan

Request a written payoff letter and confirm the balance in writing. Once you have the final number, pay off the loan and make sure the lender files a lien release with the county. Without this release, your mineral rights will remain tied up.

Option Two: Use Other Financing to Pay Off the Loan

If you cannot afford to pay it off directly, consider using other resources:

-

Pull funds from a HELOC or credit card, sell the mineral rights, then pay off your loan amount

-

Pay off the mineral rights loan with funds from a family member, sell the mineral rights, then pay them back

This clears your title and opens the door to a competitive sale, where you are in control and no longer restricted by the loan terms.

No matter which path you are on, the goal is the same: unlock the value of your minerals without falling into a legal trap. Selling a portion is the safest way to raise cash while keeping upside.

If you already signed a loan, getting out of it cleanly is the only way to move forward with a clear title and full control.

Case Study: How One Mineral Owner Got Trapped by a Mineral Rights Loan

Here’s a somewhat fictional case study that illustrates the real world problems mineral owners can face when dealing with a lender who includes a First Right of Refusal clause and uses delay tactics to maintain control:

Name: Brian

Location: Texas

Background: Brian owned a valuable mineral interest that was producing strong royalty income. He needed cash quickly to cover medical expenses and decided to take out a mineral rights loan against his royalty income. The lender included a First Right of Refusal (FRoR) clause in the contract. At the time, it seemed harmless. The lender was quick to communicate and Brian took our a loan with no issues and got paid. Brian then decided he wanted to sell the mineral rights all together.

Stage 1: The Sale Blocked by First Right of Refusal

Brian received a competitive offer to sell his mineral rights. As required by the contract, he sent formal written notice to the lender with a copy of the offer. The lender responded by saying they intended to exercise their First Right of Refusal. They waited until virtually the last day of their first right of refusal time frame.

But instead of sending an offer letter or any real documentation, they delayed. For weeks, Brian followed up, asking when he would receive the actual offer paperwork. Each time, the lender replied vaguely or not at all. Meanwhile, the original buyer grew impatient and eventually moved on to another deal.

After wasting more than a month, the lender finally told Brian they were not going to match the offer after all.

Stage 2: The Payoff Letter That Never Came

With the original buyer gone, Brian decided to move forward with a new buyer, this time focusing on paying off the loan first to avoid any future issues. He requested a written payoff amount from the lender so that he could close the transaction.

Once again, the lender stalled. Weeks went by with no written payoff letter. Brian sent multiple follow-ups by email and certified mail. When he finally reached someone on the phone, they told him the payoff quote would be sent shortly. It never came.

Without a payoff amount, the buyer could not proceed. The second buyer walked away as well.

Stage 3: The Lien Release That Was Never Filed

Eventually, Brian was able to piece together the payoff based on his original loan documents and overpaid slightly just to ensure everything was covered. He wired the funds and requested confirmation and a lien release.

The lender acknowledged receipt of the funds, but delayed filing the lien release.

Brian followed up repeatedly and was either ignored or told that it was “being processed.” Months passed. The lien remained recorded against the property. Without a release on file, no buyer would close the sale. Brian had no access to the equity in his own minerals, despite paying off the loan in full.

Eventually after additional months of time and legal threats, Brian was able to get the lien release recorded.

During that time, the lender continued to accrue interest. Brian was so exhausted by the process it wasn’t worth fighting and he just let the lender walk away with many months of additional interest and lost money he could have made by selling quickly based on his original offer.

Does the above sound exaggerated? It’s not. Trust us. Seriously.

Free Consultation

Mineral rights loans can seem like a quick and easy solution, but the fine print often tells a different story.

These agreements can create long-term problems, limit your ability to sell, and reduce the value of your minerals.

Whether you are considering a loan or already in one, it is important to understand what you are signing and what options you have.

At Texas Royalty Brokers, we work with mineral owners every day to help them make informed decisions. If you have a loan offer or an existing agreement, we can review the documents and explain the terms in simple language. If you are looking for better alternatives, we can walk you through them.

Contact us to learn more about your loan, get a second opinion, or understand the steps to move forward. We are here to help you protect the value of your mineral rights.